(GST, Income Tax, Aadhaar–PAN, and Banking Rules)

From 1st November 2025, several key regulatory and procedural changes will come into effect across GST, Income Tax, Aadhaar–PAN, and Banking rules.

These reforms are aimed at simplifying compliance, strengthening digital verification, and ensuring a more transparent tax environment.

Let’s break down all the important updates effective from this date.

🧾 GST: Major Changes Effective from 1 November 2025

1️⃣ Simplified GST Registration Scheme for Small and Low-Risk Businesses

A new optional simplified GST registration scheme will be operational from 1st November 2025 to promote ease of doing business.

Key Highlights:

- Registration shall be granted automatically within three working days from the date of application for low-riskapplicants.

- Eligible applicants are those who determine that their output tax liability on supplies to registered persons does not exceed ₹2.5 lakh per month (inclusive of CGST, SGST/UTGST, and IGST).

- The scheme allows voluntary opting in or opting out anytime.

- Nearly 96% of new GST applicants are expected to benefit from this scheme.

Impact:

This change drastically reduces approval time and manual verification for small businesses, startups, and service providers with minimal compliance risks.

2️⃣ Risk-Based Provisional Refunds for Zero-Rated Supplies

To accelerate refunds and improve working capital for exporters, the GST Council has approved risk-based provisional refunds for zero-rated supplies (exports or supplies to SEZ units/developers).

Key Points:

- Under the amended Rule 91(2) of CGST Rules, 2017, 90% of refund claimed will be sanctioned provisionallyafter system-based risk evaluation.

- Only in exceptional cases, the officer may withhold provisional refund and conduct detailed scrutiny.

- Specific categories of taxpayers (high-risk) may be excluded via separate notification.

Effective Date: 1st November 2025

Impact:

Exporters and SEZ suppliers will get quicker refunds, improving liquidity while ensuring risk-based control through automated evaluation.

3️⃣ Provisional Refund for Inverted Duty Structure (IDS)

Extending similar relief to manufacturers and traders facing input accumulation, the government has decided to allow 90% provisional refunds even for Inverted Duty Structure (IDS) cases.

Key Highlights:

- Pending formal amendment in the CGST Act, CBIC will issue instructions to grant 90% provisional refund on the basis of risk assessment.

- This mechanism will function similar to zero-rated refunds and will be operational from 1st November 2025.

Impact:

This will significantly help businesses where input tax credit exceeds output tax liability (common in manufacturing sectors).

4️⃣ Time Limit of Three Years for Filing GST Returns

As per Finance Act, 2023, implemented via Notification No. 28/2023, taxpayers will not be allowed to file GST returns after the expiry of three years from the original due date.

This restriction will be fully implemented on the GST portal from 1st November 2025.

Returns Covered:

- GSTR-1, IFF

- GSTR-3B

- GSTR-4 (Composition)

- GSTR-5, 5A (Non-residents, OIDAR)

- GSTR-6 (ISD)

- GSTR-7, 8 (TDS/TCS)

- GSTR-9 & 9C (Annual Return and Reconciliation Statement)

Example:

Any return for September 2022 or earlier that remains unfiled will be barred from filing after 1st November 2025.

Impact:

Taxpayers with pending returns should reconcile records and complete filings before the cut-off to avoid permanent blocking and compliance issues.

5️⃣ “Pending” Option for Credit Notes in IMS

A new feature has been introduced in the Invoice Management System (IMS) on the GST portal:

Key Features:

- Taxpayers can now mark Credit Notes as “Pending” for one tax period.

- Flexibility provided to revise ITC reversal once the credit note is accepted.

- Aims to reduce disputes between suppliers and recipients regarding timing and acceptance.

Impact:

Businesses now get more control in managing credit notes and ITC adjustments, ensuring smoother reconciliation.

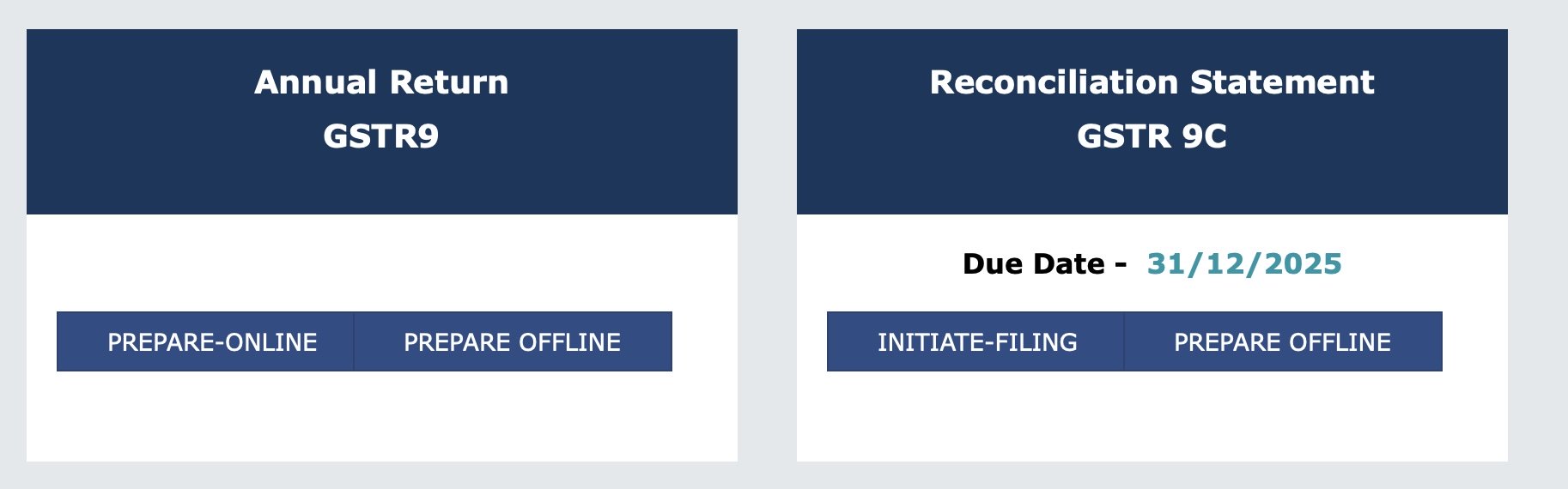

6️⃣ GSTR-9/9C Enabled for FY 2024–25

- GSTR-9 & 9C filing for FY 2024–25 is enabled on the GST portal.

- 30th November 2025 is the last date to avail ITC pertaining to FY 2024–25.

Impact:

Taxpayers should complete reconciliations and file annual returns well before the deadline to avoid missing ITC eligibility.

💼 Income Tax & Corporate Compliance Updates

While no major Income Tax rule change specifically starts on 1 November, the following compliance aspects remain critical around this period:

- 31st October 2025 – Due date for:

- Tax Audit Report

- ITR filing of companies

- ITR filing for tax audit cases and partners

- TDS Return (Q2)

- DIR-3 KYC

- 30th November 2025 – Due date for Transfer Pricing (Form 3CEB).

- 15th December 2025 – Third instalment of Advance Tax.

- 31st December 2025 – ROC Filings: AOC-4, MGT-7/7A (Annual Return and Financial Statements).

Impact:

Professionals and businesses should align audit, TDS, and ROC compliance with the new GST rule framework to ensure consistent reporting.

🪪 Aadhaar, PAN & KYC Updates

Aadhaar Updates:

- UIDAI has revised the Aadhaar update framework, allowing biometric and demographic updates at regular intervals.

- Citizens are encouraged to update Aadhaar once every 10 years to maintain accuracy.

- For minors, free biometric updates are allowed upon crossing 5 years and 15 years of age.

PAN–Aadhaar Linking:

- The final deadline for PAN–Aadhaar linking is 31st December 2025.

- Unlinked PANs will be inoperative until linked, affecting ITR filing, banking, and other financial transactions.

KYC Norms:

- Banks and financial institutions have been directed to implement real-time Aadhaar-based KYC verification.

- Enhanced periodic review for high-value accounts to prevent identity misuse and money laundering.

🏦 Banking Rule Changes (Effective Around November 2025)

- Banks will tighten monitoring of high-value cash and digital transactions with Aadhaar–PAN verification becoming mandatory.

- New KYC re-verification requirements will apply for accounts inactive for more than 2 years.

- Digital consent-based account opening norms to be introduced for faster onboarding.

- Updated credit card and UPI linking guidelines to ensure PAN verification for all linked accounts.

Visit www.cagurujiclasses.com for practical courses