")

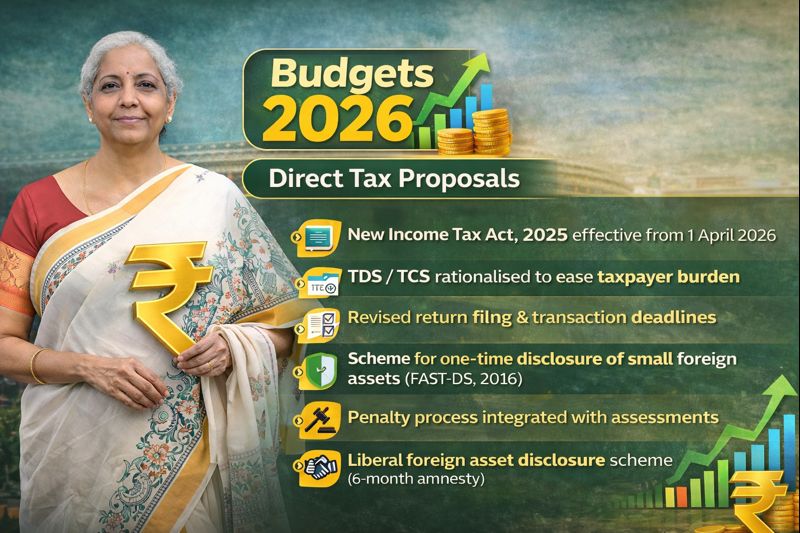

The Union Budget 2026 has introduced important reforms in the TDS and TCS framework under the Income-tax Act, 2025. These amendments primarily aim at rate rationalisation, compliance simplification, clarity in interpretation, relief to taxpayers, and partial decriminalisation.

All the changes discussed below will be effective from 1 April 2026, unless stated otherwise.

1. Rationalisation of TCS Rates – Section 394(1)

Section 394(1) earlier prescribed multiple and inconsistent TCS rates for different transactions. Budget 2026 proposes to rationalise and standardise TCS rates, wherever feasible, while also providing rate reduction relief in certain cases.

Revised TCS Rate Structure

| Sl. No. | Nature of Receipt | Current Rate | Proposed Rate |

|---|---|---|---|

| 1 | Sale of alcoholic liquor for human consumption | 1% | 2% |

| 2 | Sale of tendu leaves | 5% | 2% |

| 3 | Sale of scrap | 1% | 2% |

| 4 | Sale of minerals (coal, lignite, iron ore) | 1% | 2% |

| 5(a) | LRS remittance – education / medical treatment exceeding ₹10 lakh | 5% | 2% |

| 5(b) | LRS remittance – other purposes | 20% | 20% (unchanged) |

| 6 | Sale of “overseas tour programme package” including expenses for travel or hotel stay or boarding or lodging or any such similar or related expenditure. | (a) 5% of amount or aggregate of amounts up to ten lakh rupees (b) 20% of amount or aggregate of amounts exceeding ten lakh rupees. | 2% without threshold |

2. Overseas Tour Programme Package – Major Relief

Earlier, TCS on overseas tour packages was:

- 5% up to ₹10 lakh

- 20% above ₹10 lakh

Budget 2026 Change

- Uniform TCS rate of 2%

- Threshold of ₹10 lakh removed

- Applicable irrespective of amount

Impact

- Reduces tax burden on travellers

- Prevents business shift from Indian tour operators to overseas sellers

- Simplifies compliance for tour operators

3. Liberalised Remittance Scheme (LRS) – Rate Reduction

For remittances under RBI’s LRS:

| Purpose | Earlier TCS | New TCS |

|---|---|---|

| Education / Medical treatment (above ₹10 lakh) | 5% | 2% |

| Other purposes | 20% | No change |

This move provides significant relief to students and patients remitting funds abroad.

4. Enabling Electronic Application for Lower / Nil TDS Certificates – Section 395

Earlier Position

- Application for lower/nil TDS had to be filed manually before the Assessing Officer

- Process was time-consuming and compliance-heavy

Budget 2026 Amendment

- Payee can now apply electronically

- Application to be made before a prescribed income-tax authority

- Certificate may be:

- Issued electronically, or

- Rejected if conditions are not fulfilled / application is incomplete

Benefit

- Major compliance relief for small taxpayers

- Faster processing and transparency

5. TDS on Supply of Manpower – Ambiguity Removed

Issue Earlier

There was confusion regarding whether supply of manpower should be taxed as:

- Contract work (Section 393(1) – 1% / 2%), or

- Technical/professional services (Section 393(1) – up to 10%)

Budget 2026 Clarification

- Supply of manpower is explicitly included under “work” in Section 402(47)

- Applicable TDS:

- 1% if payee is Individual / HUF

- 2% in other cases

Result

- Litigation risk reduced

- Uniform treatment across taxpayers

6. Deduction Allowed to Non-Life Insurance Business for Late TDS Payment

Problem Earlier

- If TDS was not deducted/paid on certain expenses:

- Expense was disallowed

- But no clear mechanism to allow deduction in later year after payment

Budget 2026 Solution

- Schedule XIV amended

- New sub-paragraph proposed to allow:

- Deduction in the year in which TDS is deducted and paid

Applicability

- Non-life insurance business

- Effective from AY 2026–27 onwards

7. Decriminalisation & Rationalisation of TDS/TCS Offences – Section 476 & 477

Fully Decriminalised Offences

Failure to deposit TDS related to:

- Lottery / crossword puzzle winnings

- Benefits or perquisites arising from business or profession

➡️ No imprisonment

Modified Punishment Structure for Certain Cases

For:

- Online gaming winnings

- Virtual digital asset (VDA) transactions

| Amount of TDS Default | Punishment |

|---|---|

| Exceeds ₹50 lakh | Simple imprisonment up to 2 years / fine / both |

| ₹10 lakh – ₹50 lakh | Simple imprisonment up to 6 months / fine / both |

| Other cases | Fine only |

Wholly in-kind transactions (online games & VDA) are excluded from prosecution.

8. TDS on Sale of Immovable Property by Non-Resident – Procedural Relief

Earlier

- Buyer had to obtain TAN for TDS compliance

Now

- TDS to be deducted and deposited using:

- Resident buyer’s PAN-based challan

- No TAN required

Impact

- Simplifies property transactions with NRIs

- Reduces compliance hurdles for buyers

Effective Date of All Amendments

✔ 1 April 2026

✔ Applicable from Tax Year 2026–27 onwards

Taxpayers, professionals, tour operators, insurers, and businesses dealing with manpower supply or foreign remittances must realign their systems and contracts well before 1 April 2026.

Visit www.cagurujiclasses.com for practical courses