The Central Board of Direct Taxes (CBDT) has released a circular (13/2025) wherein certain benefit has been given to those who claimed Section 87A tax rebate for special rate income like short term capital gains (STCG) on sale of equities and got a tax notice with demand.

According to this circular, if you had claimed Section 87A tax rebate on special rate income like STCG on equities and this claimed was accepted also, then you can get a tax demand notice. However, if you pay this tax demand by December 31, 2025 then any penal interest if levied will be waived. If you don’t pay the tax demand by December 31, 2025 for such Section 87A tax rebate cases then the interest will be levied.

Expert said to ET Wealth Online: “This circular provides indication to those taxpayers who could have claimed Section 87A tax rebate on STCG income prior to July 5, 2024. These taxpayers will get a tax notice for claiming Section 87A tax rebate. After judgment of Bombay High Court for restricting 87A claim in ITR and several lower court judgments allowing 87A, relief was expected from income tax department. However, by issuing this circular department, it is clear that litigation on 87A is likely to increase. Circular give marginal relief that even if tax payer doesn’t pay demand within 30 days of receiving this tax notice, interest at 1% per month will not be payable. This present circular (13/2025) has waived off the interest, if the taxpayer pays the tax demand on or before December 31, 2025.”

What did CBDT say in the circular?

CBDT in the circular (13/2025) dated September 19, 2025 said the following:

- The provisions of Section 115BAC(1A) of the Income-tax Act, 1961 are subject to the other provisions of Chapter XII. Therefore, incomes chargeable to tax at special rates specified under various provisions of Chapter XII are not included while determining the chargeability to tax under Section 115BAC(1A). Further, the clause (b) of proviso to Section 87A is applicable to incomes chargeable to tax under Section 115BAC(1A).

- It is noticed that in certain cases, the returns had already been processed and rebate was allowed under Section 87A on incomes chargeable to tax at special rates. In such cases, rectifications have to be carried out to disallow such Section 87A tax rebate, which has been incorrectly allowed. Such rectifications will result in demands getting raised. If the payments of such demands raised are delayed then the same are liable for charging of interest under Section 220 (2).

- In order to mitigate the genuine hardship arising to such taxpayers on account of interest payable under Section 220 (2), the CBDT in exercise of its powers conferred under Section 119, directs that the interest payable under Section 220(2) shall be waived in such cases where the payment of the tax demands raised, is made on or before December 31, 2025.

- In such cases, if a taxpayer fails to pay the tax demand raised as a result of rectification order passed by the CPC on or before December 31, 2025, the interest shall be charged under Section 220(2) from the day immediately following the end of the period mentioned in sub-section (1) of Section 220.

Also read: Father sold family land for daughter’s marriage; first son alleged father was alcoholic and filed a case but lost in Supreme Court due to this reason

What is the issue that is causing such problems regarding claiming of 87A tax rebate

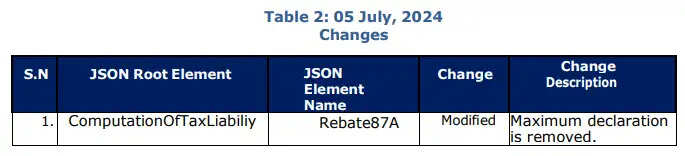

According to an earlier Economic Times report dated July 21, 2024, the ITR filing utilities stopped allowing tax rebate under section 87A for various special rate incomes including short-term capital gains on equity shares or equity-oriented mutual funds taxable at 15% under Section 111A.

“Earlier the Income Tax Utility Software allowed filing of ITRs with rebate, but after July 5, 2024, a whole controversy arose due to change of schema of utility software by the income tax department. Pursuant to those ITRs which were filed with tax rebate are now getting intimation notices for tax demand equivalent to amount to rebate availed. Recently, more than 500 demand notices were received by members of Chartered Accountants Association Surat. Where there was a refund due, the amount of rebate was deducted from it after processing of the ITR,” said Expert

Once the rebate facility was stopped, taxpayers could not claim 87A rebate in conjunction with the special tax rate like STCG. Many people were previously allowed to make this claim, and now they are receiving tax demand notices as a result. “Those taxpayers who have claimed rebate, using old utility or adjusting 87A rebate amount, are now getting a tax notice wherein tax demand is raised with reduced amount of rebate,” said Expert

Visit www.cagurujiclasses.com for practical courses