The calculation of tax rebates continues to be unclear when it comes to income from capital gains. This issue arises following finance minister Nirmala Sitharaman’s decision to increase the tax-rebate threshold under Section 87A of the Income Tax Act from ₹7 lakh to ₹12 lakh in the Union Budget 2025-26.

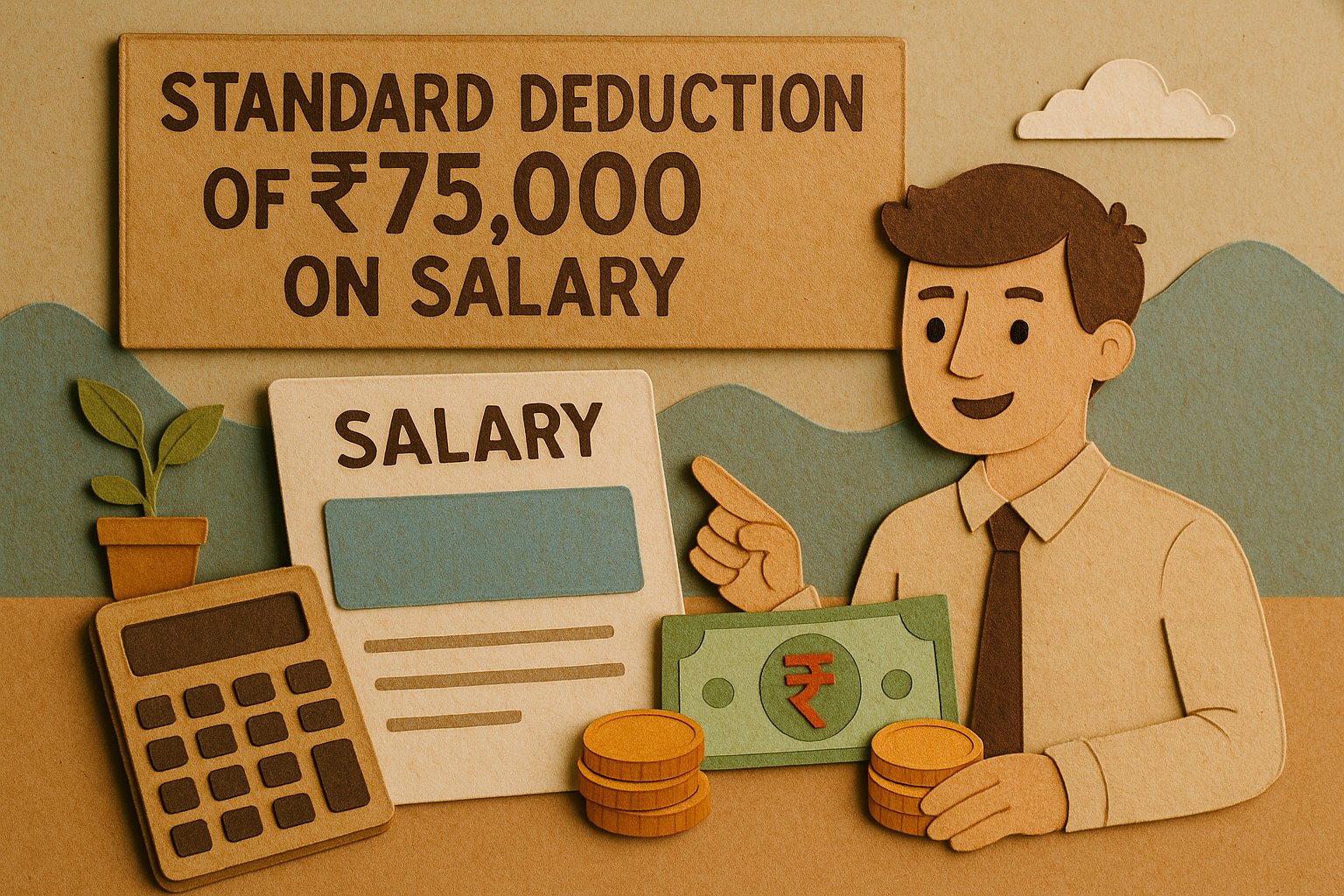

When taking into account, the standard deduction of ₹75,000, the actual threshold becomes ₹12.75 lakh for salaried individuals.

However, this raises the question of what happens if a person with a ₹12 lakh salary earns an extra ₹1 lakh from capital gains.

“Since capital gains are classified as special-rate income, they do not qualify for the rebate,” Live Mint reported quoted V Rajitha, the official spokesperson of the Central Board of Direct Taxes (CBDT) as saying. “However, their impact on overall tax liability depends on the way the rebate is structured — whether it is based solely on normal income or the total taxable income.”

“If the rebate applies only to normal income, an individual with a ₹12 lakh salary and any additional capital gains should still be eligible for the rebate on salary income,” she added. “However, if capital gains are included when determining whether a person is eligible for a rebate, then exceeding ₹12 lakh may disqualify him from the rebate. The Finance Bill’s specific language will determine this aspect.”

The exact same confusion however, also exists under the current rules. “Under existing provisions, the Section 87A rebate applies if total income (including capital gains) is below ₹7 lakh, and capital gains are taxed separately. However, If capital gains push total income above ₹7 lakh, the rebate may not be available,” the report added.

Visit www.cagurujiclasses.com for practical courses

Pla clarify the point whether rebate would still be available in the above case. Yes or no