CBDT Notifies ITR Form 2 for AY 2025-26

The Central Board of Direct Taxes (CBDT) has officially notified Income Tax Return (ITR) Form 2 for Assessment Year 2025–26, vide Notification No. 43/2025 dated 03.05.2025.

This form is applicable for individuals and HUFs not having income from business or profession. Several key changes have been introduced to align with amendments made by the Finance Act, 2024.

Key Updates in ITR Form 2:

Key Updates in ITR Form 2:

Capital Gains Split:

Capital Gains Split:

Schedule-Capital Gain now bifurcates gains before and after 23.07.2024, to accommodate tax changes introduced by the Finance Act, 2024.

Capital Loss on Buyback Allowed:

Loss on share buyback is now allowed post 01.10.2024, provided the corresponding dividend income is declared under ‘Income from Other Sources’.

Asset & Liability Threshold Revised:

The limit for mandatory reporting of assets and liabilities has been increased to ₹1 crore of total income.

Detailed Deduction Reporting:

Enhanced disclosure required for deductions under Section 80C, House Rent Allowance [Section 10(13A)], and others.

TDS Section Code Reporting:

Taxpayers must now report the relevant TDS section code in Schedule-TDS, improving traceability and compliance.

Official Notification & Details:

Official Notification & Details:

Click here to view the Gazette Notification

You can contact team of Tax Experts to file Your ITR at 9150010300 or visit www.legalsahayak.com

ITR 1 & ITR 4 already notified:

Visit www.cagurujiclasses.com for practical courses

Traces: New Utility for Justification Report, Form 16A and Form 27D Released

Traces: New Utility for Justification Report, Form 16A and Form 27D Released

Delay in ITR Filing Utilities: Why Only ITR-1/4 Are Available So Far? When ITR-2/3 available?

Delay in ITR Filing Utilities: Why Only ITR-1/4 Are Available So Far? When ITR-2/3 available?

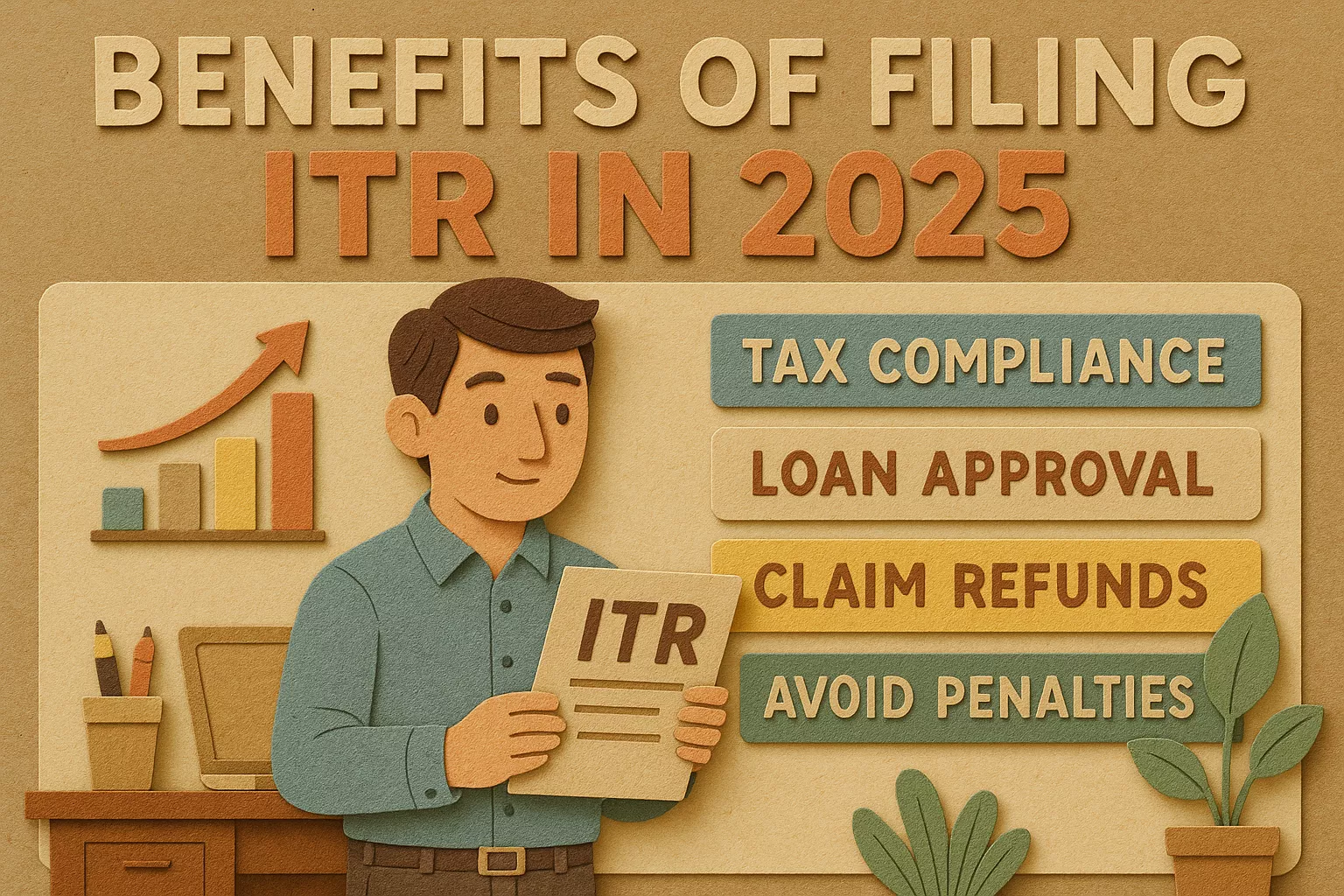

50+ Benefits of Filing ITR in 2025

50+ Benefits of Filing ITR in 2025

Compliance Calendar for July 2025

Compliance Calendar for July 2025