As by Budget 2024 Government bring change in Capital Gain Taxation from 23 July 2024, which is the most discussed topic after the budget having various doubts and issues in the new tax rates so now Government issued clarification w.r.t property bought before 2001 by tweet as below:

Clarification by Income Tax India on Property Bought Before 2001

New Capital Gains Taxation regime

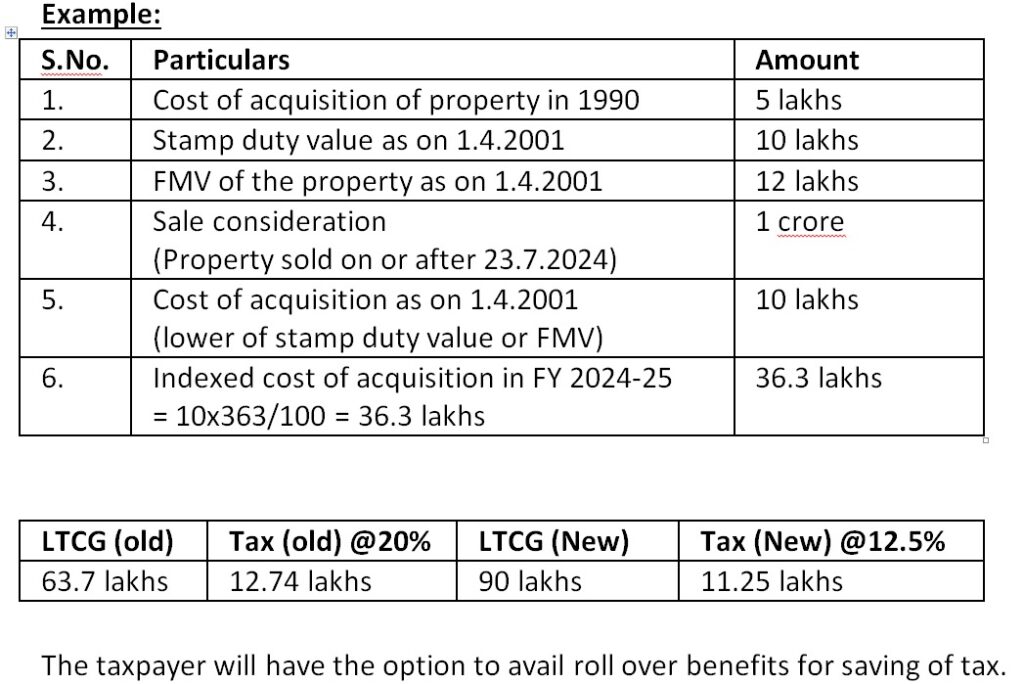

An issue has been raised as to what would be the Cost of Acquisition as on 1.4.2001 for properties purchased prior to 2001.

For properties (land or building or both) purchased prior to 1.4.2001, the cost of acquisition as on 1.4.2001 shall be:-

- Cost of Acquisition of the asset to the assesse; or

- the Fair Market Value (not exceeding the stamp duty value, wherever available) of such asset as on 1.4.2001.

Taxpayers can choose either option as per section 55(2)(b) of the Income-tax Act, 1961.

below is Section 55(2)(b) of Income tax Act:

(b) in relation to any other capital asset,—

(i) where the capital asset became the property of the assessee before the 1st day of April, 2001, means the cost of acquisition of the asset to the assessee or the fair market value of the asset on the 1st day of April, 2001, at the option of the assessee;

(ii) where the capital asset became the property of the assessee by any of the modes specified in sub-section (1) of section 49, and the capital asset became the property of the previous owner before the 1st day of April, 2001, means the cost of the capital asset to the previous owner or the fair market value of the asset on the 1st day of April, 2001, at the option of the assessee:

Provided that in case of a capital asset referred to in sub-clauses (i) and (ii), being land or building or both, the fair market value of such asset on the 1st day of April, 2001 for the purposes of the said sub-clauses shall not exceed the stamp duty value, wherever available, of such asset as on the 1st day of April, 2001.

Explanation.—For the purposes of this proviso, “stamp duty value” means the value adopted or assessed or assessable by any authority of the Central Government or a State Government for the purpose of payment of stamp duty in respect of an immovable property;

(iii) where the capital asset became the property of the assessee on the distribution of the capital assets of a company on its liquidation and the assessee has been assessed to income-tax under the head “Capital gains” in respect of that asset under section 46, means the fair market value of the asset on the date of distribution;

(iv) [***]

(v) where the capital asset, being a share or a stock of a company, became the property of the assessee on—

(a) the consolidation and division of all or any of the share capital of the company into shares of larger amount than its existing shares,

(b) the conversion of any shares of the company into stock,

(c) the re-conversion of any stock of the company into shares,

(d) the sub-division of any of the shares of the company into shares of smaller amount, or

(e) the conversion of one kind of shares of the company into another kind,

means the cost of acquisition of the asset calculated with reference to the cost of acquisition of the shares or stock from which such asset is derived.

To know the other changes related to capital Gain Tax on property and other watch below videos

Visit www.cagurujiclasses.com for practical courses

The new LTCG tax is not capital gain tax, but in reality it is going to be capital erosion tax or tax on capital loss.

If I invest some money in FD , it would fetch more returns than the new capital gain tax.

The investor mostly middle class community builds a house with great difficulties, will end up paying heavy tax .

This tax is worse than Congress party’s proposed inheritance tax.

If what government says is true that the new tax structure is for simplification, then government shall prove its argument by giving two options with and without indexation benefit like old tax regime and new tax regime.

Government in any way doesn’t loose revenue,as it claims.

The alternative can be to reduce tax level to 3 % instead of 12.5%

We need atleast one learned person who can clarify this.i don’t think any section of the Act speaks about this…will stand corrected if I am wrong….

Question

“Can the assessee do indexation of property if the land is allotted free of cost by the government before 1981”

Everyone speaks about LTCG especially in the last few days…can someone clarify this

Thanks for the details kindly cnf whether capital bond scheme still in force. I have sold my flat on 27th June. Property was acquired in 1982 and the govt valuator jss valued it as on 2001 at rs 10.80 lacs

Please guide me