The Union Budget 2024 presented on 23 July 2024 has introduced changes to the capital gain tax rates.

Memorandum: Rationalisation and Simplification of Taxation of Capital Gains

The taxation of capital gains is proposed to be rationalized and simplified. There are three components to this simplification:

- Holding Periods:

- Proposed Changes:

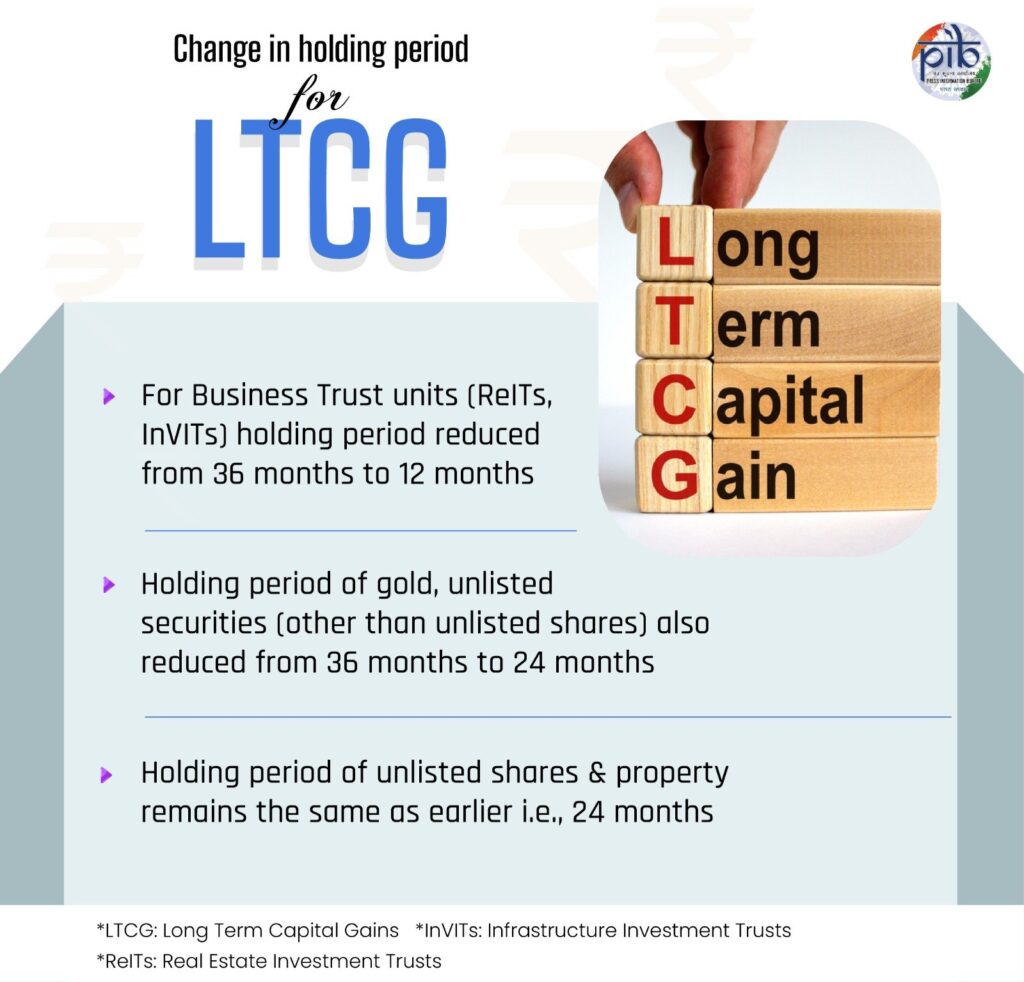

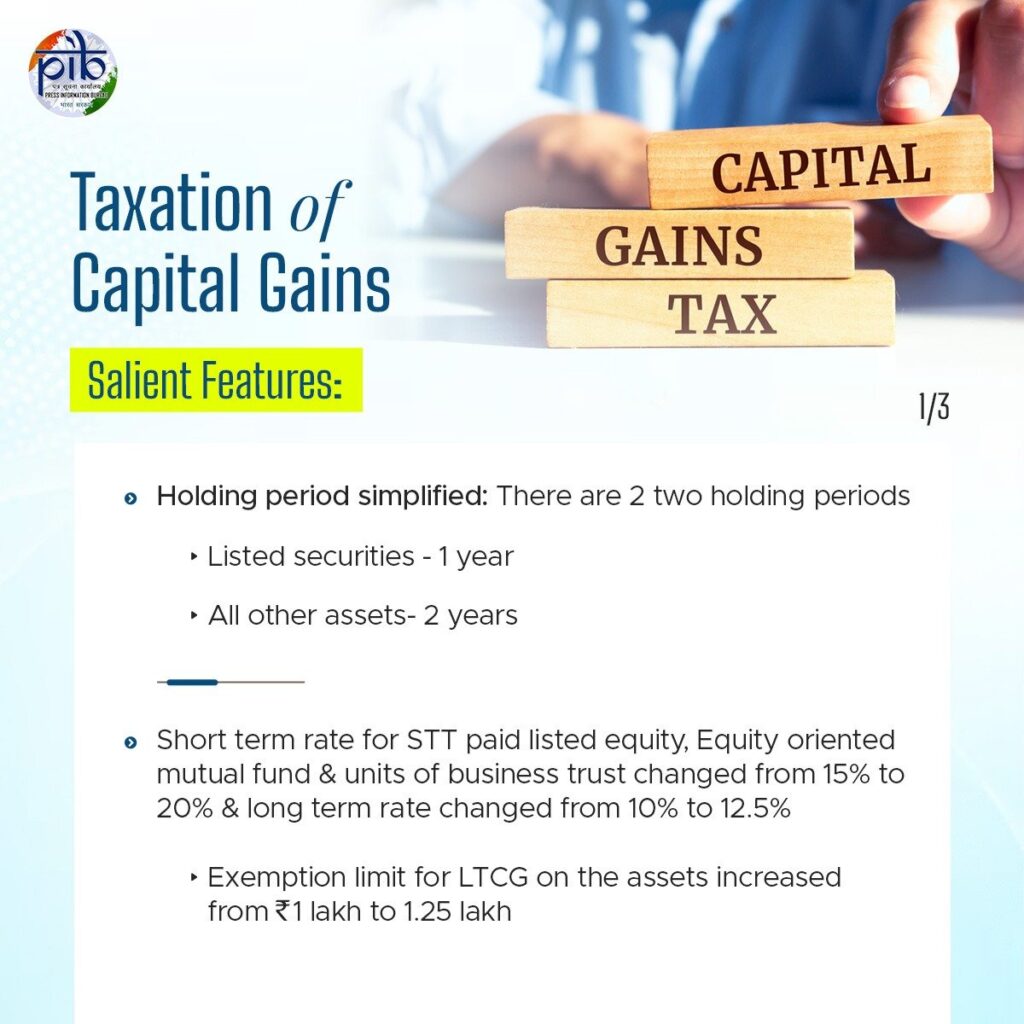

- Only two holding periods: 12 months and 24 months.

- For all listed securities, the holding period is proposed to be 12 months.

- For all other assets, the holding period shall be 24 months.

- Amendments:

- Amendment is proposed in clause (42A) of section 2 of the Act.

- Units of listed business trust will now be at par with listed equity shares at 12 months instead of the earlier 36 months.

- The holding period for bonds, debentures, and gold will reduce from 36 months to 24 months.

- For unlisted shares and immovable property, it shall remain at 24 months.

- Proposed Changes:

- Short-Term and Long-Term Capital Gains Rates:

- Short-Term Capital Gains:

- The rate for short-term capital gain under provisions of section 111A of the Act on STT paid equity shares, units of equity-oriented mutual funds, and units of a business trust is proposed to be increased to 20% from the present rate of 15%.

- Other short-term capital gains shall continue to be taxed at the applicable rate.

- Long-Term Capital Gains:

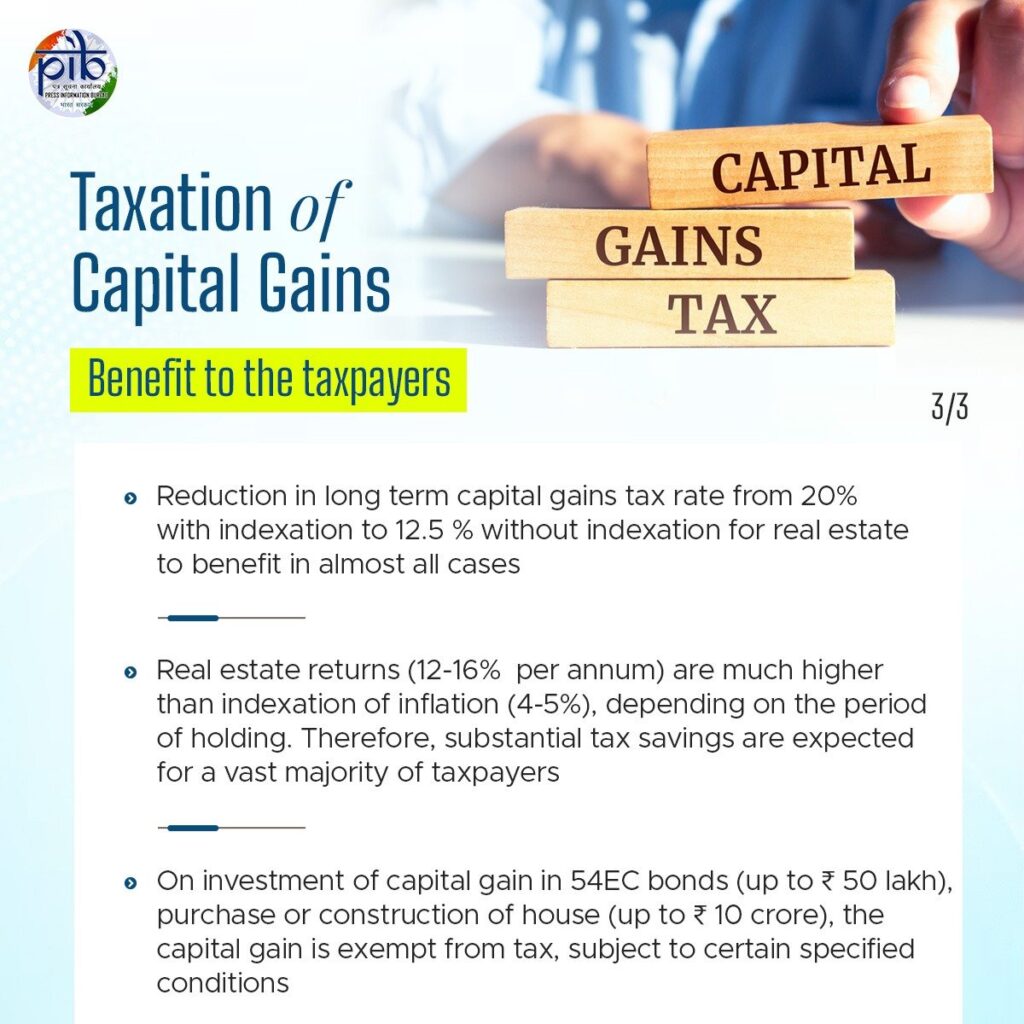

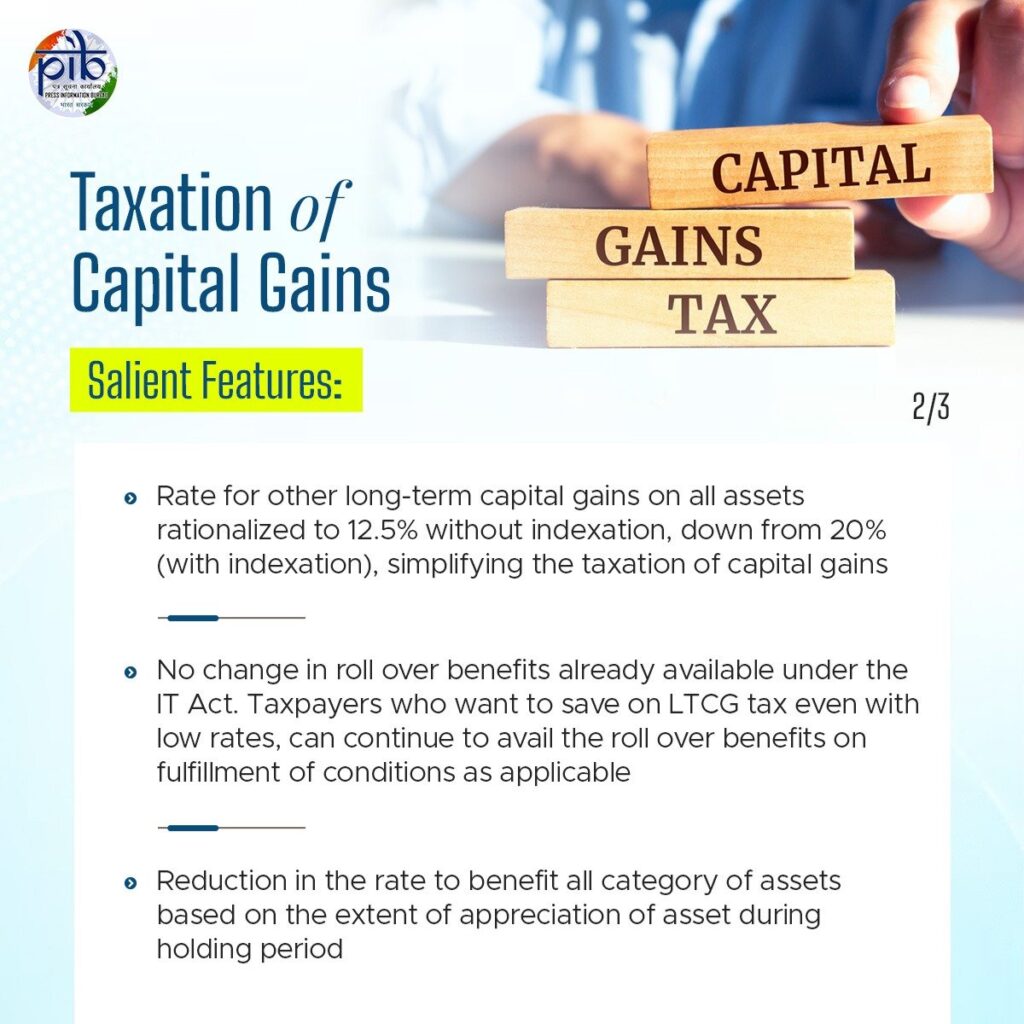

- The rate of long-term capital gains under various sections of the Act is proposed to be 12.5% for all categories of assets.

- Earlier, it was 10% for STT paid listed equity shares, units of equity-oriented funds, and business trusts under section 112A, and 20% with indexation under section 112 for other assets.

- An exemption of gains up to 1.25 lakh (aggregate) is proposed for long-term capital gains under section 112A on STT paid equity shares, units of equity-oriented funds, and business trusts, increasing the previously available exemption of up to 1 lakh of income from long-term capital gains on such assets.

- For bonds and debentures, the rate for taxation of long-term capital gains was 20% without indexation. For listed bonds and debentures, the rate shall be reduced to 12.5%.

- Unlisted debentures and unlisted bonds, being of the nature of debt instruments, should be taxed at the applicable rate, whether short-term or long-term.

- Short-Term Capital Gains:

- Indexation Removal:

- Simultaneously with the rationalization of the rate to 12.5%, indexation available under the second proviso to section 48 is proposed to be removed for the calculation of any long-term capital gains, which is presently available for property, gold, and other unlisted assets.

- This will ease the computation of capital gains for the taxpayer and the tax administration.

- Parity in Taxation:

- To bring parity between resident and non-resident assesses, corresponding amendments to sections 115AD, 115AB, 115AC, 115ACA, and 115E are being made to align the rates of taxation in respect of long-term capital gains proposed under sections 112A and 112, and rates of short-term capital gains proposed under section 111A.

- Withholding Tax Provisions:

- Consequential amendments to align the withholding tax provisions with the substantive provisions are being made under sections 196B and 196C to give effect to the proposed changes in rates of capital gains tax.

- Effective Date:

- These proposals are proposed to be given effect immediately, i.e., with effect from the 23rd of July, 2024.

Comparison Table:

| Aspect | Current Regulation | Proposed Regulation |

|---|---|---|

| Holding Period for Long-Term Capital Gains | Listed Securities: 12 months Other Assets: 36 months | Listed Securities: 12 months Other Assets: 24 months |

| Holding Period for Specific Assets | Units of Listed Business Trust: 36 months Bonds, Debentures, Gold: 36 months Unlisted Shares, Immovable Property: 24 months | Units of Listed Business Trust: 12 months Bonds, Debentures, Gold: 24 months Unlisted Shares, Immovable Property: 24 months |

| Short-Term Capital Gains Tax Rate (Section 111A) | STT Paid Equity Shares, Units of Equity-Oriented Mutual Funds, Business Trusts: 15% | STT Paid Equity Shares, Units of Equity-Oriented Mutual Funds, Business Trusts: 20% |

| Long-Term Capital Gains Tax Rate (Section 112A) | STT Paid Listed Equity Shares, Units of Equity-Oriented Funds, Business Trusts: 10% | All Assets: 12.5% |

| Long-Term Capital Gains Tax Rate (Section 112) | Other Assets: 20% with indexation | All Assets: 12.5% |

| Exemption on Long-Term Capital Gains (Section 112A) | STT Paid Equity Shares, Units of Equity-Oriented Funds, Business Trusts: Up to ₹1 lakh | STT Paid Equity Shares, Units of Equity-Oriented Funds, Business Trusts: Up to ₹1.25 lakh |

| Tax Rate for Bonds and Debentures | Long-Term Capital Gains: 20% without indexation | Listed Bonds and Debentures: 12.5% Unlisted Debentures and Bonds: Applicable rate (short-term or long-term) |

| Indexation for Long-Term Capital Gains | Available for Property, Gold, and Other Unlisted Assets | Removed for Property, Gold, and Other Unlisted Assets |

| Tax Parity Between Residents and Non-Residents | Different rates for various sections | Aligned rates under sections 115AD, 115AB, 115AC, 115ACA, and 115E with sections 112A and 112 for long-term capital gains and section 111A for short-term capital gains |

| Withholding Tax Provisions | Existing provisions under sections 196B and 196C | Aligned with new rates under sections 196B and 196C |

| Effective Date | – | 23rd July 2024 |

Short Term Capital Gain:

Budget Speech – Simplification of taxation of Capital Gains: The taxation of capital gains is proposed to be rationalised and simplified.

Short term gains on specified financial assets shall henceforth attract a tax rate of 20 per cent instead of 15 per cent, while that on all other financial assets and non-financial assets shall

continue to attract the applicable tax rate.

Finance Bill:

Long Term Capital Gain:

Budget Speech:

Long term gains on all financial and non-financial assets, on the other hand, will attract a tax rate of 12.5 per cent. For the benefit of the lower and middle-income classes, it is proposed to increase

the limit of exemption of capital gains on certain listed financial assets from ₹ 1 lakh to ₹ 1.25 lakh per year.

Finance Bill:

Revision of Rates of Securities Transaction Tax by Amendment to the Finance (No.2) Act, 2024

- Introduction of Securities Transaction Tax (STT)

- The levy of Securities Transaction Tax (STT) on transactions in specified securities was introduced via the Finance (No.2) Act, 2004.

- Recognized stock exchanges, mutual funds (having equity-oriented schemes), insurance companies, or lead merchant bankers appointed by the company in respect of an initial public offer or initial offer are liable to collect the tax on specified securities.

- The collected STT must be paid to the credit of the Central Government within seven days from the end of the month in which it is collected.

- The rates of STT have been revised periodically since its introduction in 2004.

- Current Rates of STT

- The rate of levy on the sale of an option in securities: 0.0625% of the option premium.

- The rate of levy on the sale of a future in securities: 0.0125% of the price at which such “futures” are traded.

- The rate of levy on delivery trades in equity shares: 0.1% on both purchase and sale transactions.

- The rate of levy on the sale of an option in securities where the option is exercised: 0.125% of the intrinsic price (the difference between the settlement price and the strike price), payable by the purchaser.

- Proposed Changes Due to Derivative Market Growth

- Due to the exponential growth of derivative (future and option) markets, which now account for a significant portion of trading in stock exchanges, it is proposed to increase the STT rates.

- Proposed new rates:

- Sale of an option in securities: from 0.0625% to 0.1% of the option premium.

- Sale of futures in securities: from 0.0125% to 0.02% of the price at which such “futures” are traded.

- Effective Date

- The proposed amendments are to be made effective from the 1st day of October, 2024.

| Aspect | Current Regulation | Proposed Regulation |

|---|---|---|

| Introduction and Collection of STT | Introduced via Finance (No.2) Act, 2004. | No change. |

| Entities Liable to Collect STT | Recognized stock exchanges, mutual funds (equity-oriented schemes), insurance companies, or lead merchant bankers for IPOs. | No change. |

| Payment Deadline | Within seven days from the end of the month in which STT is collected. | No change. |

| STT on Sale of an Option in Securities | 0.0625% of the option premium. | 0.1% of the option premium. |

| STT on Sale of a Future in Securities | 0.0125% of the price at which futures are traded. | 0.02% of the price at which futures are traded. |

| STT on Delivery Trades in Equity Shares | 0.1% on both purchase and sale transactions. | No change. |

| STT on Sale of an Option in Securities (if exercised) | 0.125% of the intrinsic price (difference between settlement price and strike price), payable by the purchaser. | No change. |

| Reason for Changes | N/A | Exponential growth in derivative markets. |

| Effective Date | N/A | 1st October 2024. |

Visit www.cagurujiclasses.com for practical courses

मैने मई 2024 में अपना आवासीय घर 11000000/₹ में बेचा जो मेरे पिता ने 1983 में खरीदा था और उसे 2015 में UIT के जरिए रजिस्टर्ड करवाया जिसमे प्लाट की कीमत (#पूर्व मे 2700000/₹ )..लिखी गई

कृपया बताइए कि इस पर कैपिटल गेन टैक्स इंडेक्सेशन लगेगा या नही ..अगर हां तो कौनसे साल से..और कैसे..🙏🙏