The Finance Act 2021 ushered in a significant change in India’s tax regime with the introduction of Section 194P, aimed at providing relief to senior citizens from the burdensome process of filing income tax returns. This provision targets individuals aged 75 years and above, acknowledging their contribution to society and their evolving financial needs in their twilight years.

Understanding Section 194P:

Section 194P of the Income-tax Act, 1961, introduced in Budget 2021, delineates the conditions under which senior citizens aged 75 years and above are exempted from filing income tax returns. Traditionally, Section 139 of the Income Tax Act mandated the filing of returns by individuals surpassing the basic exemption limit.

However, in a bid to alleviate the compliance burden for elderly taxpayers, the Union Budget 2021 brought forth this exemption, subject to specific criteria:

- Age Criterion: Senior citizens must be 75 years or older.

- Residency Status: They should be ‘Resident’ in the previous year.

- Income Sources: The individual must derive income solely from pension and interest earned from a bank account (savings or deposits), with the interest accrued from the same bank where the pension is received.

Conditions for Exemption under Section 194P:

To avail of the exemption, senior citizens need to submit a declaration containing essential details to their respective banks, which must be specified by the Central Government. These specified banks will then be tasked with deducting TDS for eligible senior citizens, factoring in deductions under Chapter VI-A and rebates under Section 87A.

Filing a Declaration:

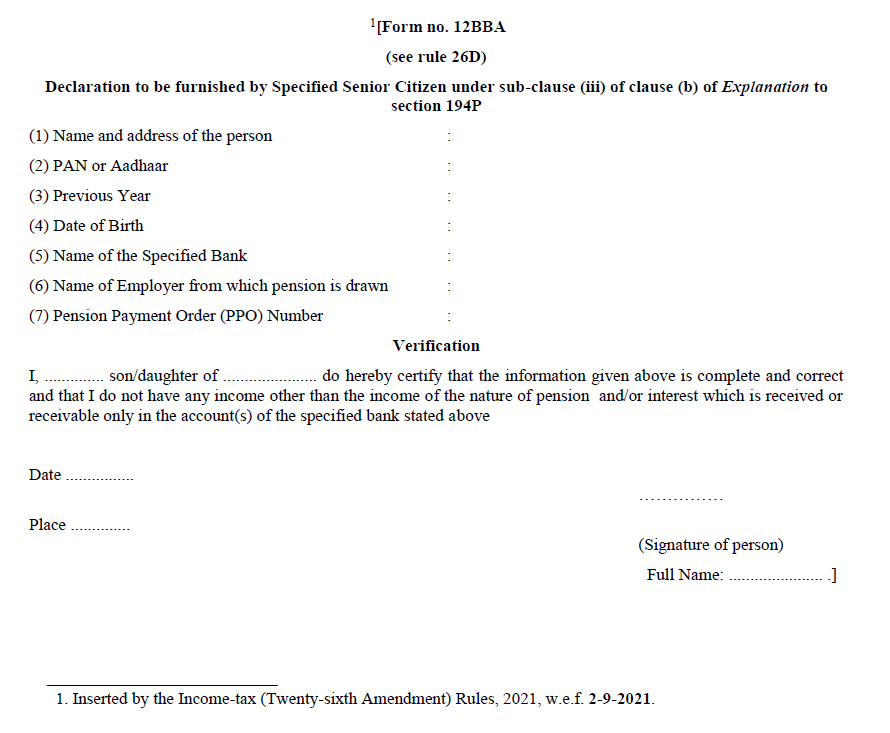

Senior citizens must furnish a declaration to the specified bank, which includes details such as PAN, Pension Payment Order (PPO) Number, total income, deductions under Section 80C to 80U, rebate under Section 87A, and confirmation of having only pension and interest income.

Calculation of Taxable Income:

Upon submission of the declaration, the bank calculates the gross total income, incorporating pension and interest income, along with deductions and rebates applicable to senior citizens. This computation aids in determining the net taxable income, against which TDS is deducted.

Benefits and Implications:

The implementation of Section 194P streamlines the taxation process for elderly citizens, relieving them of the obligation to file income tax returns. The TDS deducted by the specified bank is duly reported to the department, thus negating the need for further compliance from senior citizens aged 75 years and above.

FAQs:

1. Who is exempted from ITR filing under Section 194P? Senior citizens aged 75 years or more, deriving income solely from pension and interest from the same bank, are exempted upon submission of a declaration in Form 12BBA.

2. Which tax regime applies while deducting TDS under Section 194P? The bank calculates net taxable income considering deductions and applies the beneficial tax regime, arriving at the TDS to be made under Section 194P.

3. What are the deduction limits under Sections 80C and 80D for senior citizens? Senior citizens can avail deductions up to Rs 1,50,000 under Section 80C and up to Rs 1,00,000 under Section 80D.

4. What is Form 15H for senior citizens? Form 15H is a self-declaration form submitted to the payer to avoid TDS deduction if income falls below the basic exemption limit.

5. What is the age limit for Section 194P? The relaxation from filing ITR is available to resident senior citizens aged 75 years or older.

In essence, Section 194P stands as a testament to the government’s commitment to easing the tax compliance burden for the elderly populace, ensuring their financial well-being and security in their golden years.

Visit www.cagurujiclasses.com for practical courses

A person aged 75 years can get exemption from filing IT return provided he has no other income except pension and interest on bank deposit subject to other conditions, as per the rules made.Seemingly it appears to be a great benefit for the old.Practically, it is very difficult to fulfill the requisite conditions.During the period of 75 years, the possibility of having more than a single bank account and income from such accounts, may not be in the memory of many old aged people who generally forget such income/bank details and deposits.As such hardly any people can fulfill the relevant conditions to avail of this benefit.The number of beneficiaries will certainly be indicative of the use.

Incomtax.refund.pension.whichdate

This is very funny . What is percentage of people who can live upto and after 75 years in India with the available public health care unless one is rich enough to spend few lakhs of Rupees at a corporate hospitals.

Is the income occured from the deposite in finance institutions such as Govt. Run power finance co. is exempted?