The Union Budget 2024 introduced sweeping changes to the taxation of capital gains, particularly impacting those who own property. While the reduction in the long-term capital gains (LTCG) tax rate from 20% to 12.5% appears beneficial, the simultaneous removal of indexation benefits has thrown a spanner in the works, especially for property owners.

Understanding Indexation Benefits

Before we delve into the implications of the new tax regime, let’s clarify what indexation means. Essentially, it’s a method to adjust the purchase price of an asset for inflation over the years. This adjusted price is then used to calculate capital gains, effectively reducing the taxable profit.

For instance, if you bought a property in 2005 for Rs. 10 lakh and sold it in 2024 for Rs. 50 lakh, the actual profit might seem substantial. However, due to inflation, the purchasing power of Rs. 10 lakh in 2005 is not the same as Rs. 10 lakh in 2024. Indexation helps account for this difference, thereby reducing the taxable gain.

The New Tax Regime: A Double-Edged Sword

The Budget 2024 has introduced a dual impact on property sellers:

- Reduced LTCG Tax Rate: The LTCG tax rate has been slashed from 20% to 12.5%, which is undoubtedly a positive development.

- Removal of Indexation Benefits: This is where the catch lies. While the tax rate is lower, the removal of indexation means that the entire difference between the purchase price and sale price becomes taxable, irrespective of inflation.

Clarification by Income Tax India on Property Bought Before 2001

New Capital Gains Taxation regime

An issue has been raised as to what would be the Cost of Acquisition as on 1.4.2001 for properties purchased prior to 2001.

For properties (land or building or both) purchased prior to 1.4.2001, the cost of acquisition as on 1.4.2001 shall be:-

- Cost of Acquisition of the asset to the assesse; or

- the Fair Market Value (not exceeding the stamp duty value, wherever available) of such asset as on 1.4.2001.

Taxpayers can choose either option as per section 55(2)(b) of the Income-tax Act, 1961.

below is Section 55(2)(b) of Income tax Act:

(b) in relation to any other capital asset,—

(i) where the capital asset became the property of the assessee before the 1st day of April, 2001, means the cost of acquisition of the asset to the assessee or the fair market value of the asset on the 1st day of April, 2001, at the option of the assessee;

(ii) where the capital asset became the property of the assessee by any of the modes specified in sub-section (1) of section 49, and the capital asset became the property of the previous owner before the 1st day of April, 2001, means the cost of the capital asset to the previous owner or the fair market value of the asset on the 1st day of April, 2001, at the option of the assessee:

Provided that in case of a capital asset referred to in sub-clauses (i) and (ii), being land or building or both, the fair market value of such asset on the 1st day of April, 2001 for the purposes of the said sub-clauses shall not exceed the stamp duty value, wherever available, of such asset as on the 1st day of April, 2001.

Explanation.—For the purposes of this proviso, “stamp duty value” means the value adopted or assessed or assessable by any authority of the Central Government or a State Government for the purpose of payment of stamp duty in respect of an immovable property;

(iii) where the capital asset became the property of the assessee on the distribution of the capital assets of a company on its liquidation and the assessee has been assessed to income-tax under the head “Capital gains” in respect of that asset under section 46, means the fair market value of the asset on the date of distribution;

(iv) [***]

(v) where the capital asset, being a share or a stock of a company, became the property of the assessee on—

(a) the consolidation and division of all or any of the share capital of the company into shares of larger amount than its existing shares,

(b) the conversion of any shares of the company into stock,

(c) the re-conversion of any stock of the company into shares,

(d) the sub-division of any of the shares of the company into shares of smaller amount, or

(e) the conversion of one kind of shares of the company into another kind,

means the cost of acquisition of the asset calculated with reference to the cost of acquisition of the shares or stock from which such asset is derived.

To know the other changes related to capital Gain Tax on property and other watch below videos

Watch Example given by Revenue Secretary – Mr. Sanjay Malhotra

As Per Tweet of Income Tax:

Benefit of change in rate from 20% (with indexation) to 12.5% (without indexation) in real estate

- The reduction in long term capital gains tax rate from 20% with indexation to 12.5 % without indexation for real estate will benefit in almost all cases.

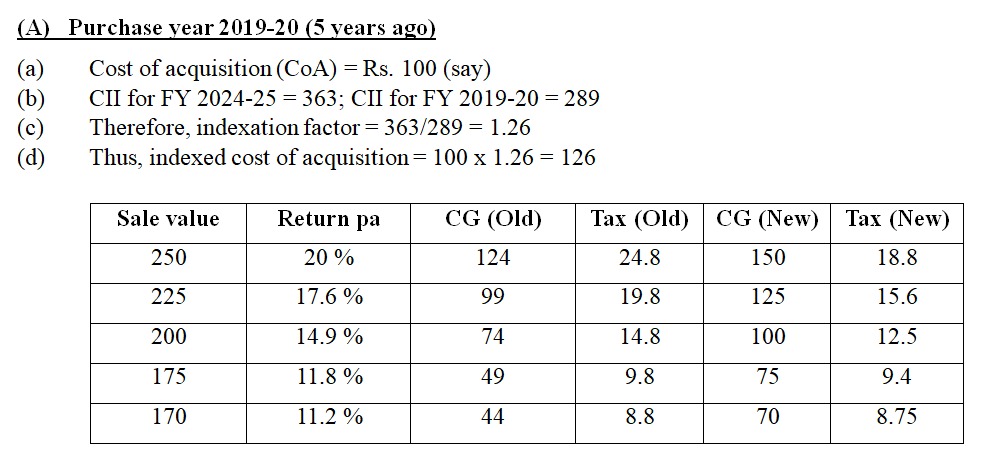

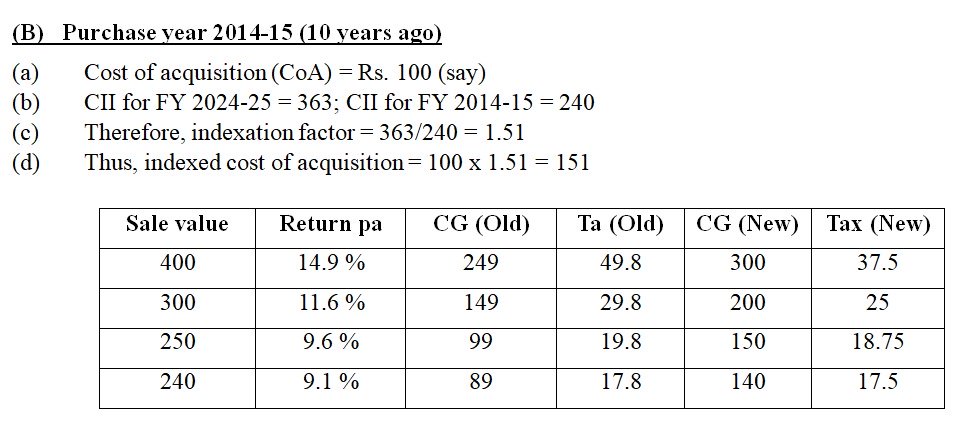

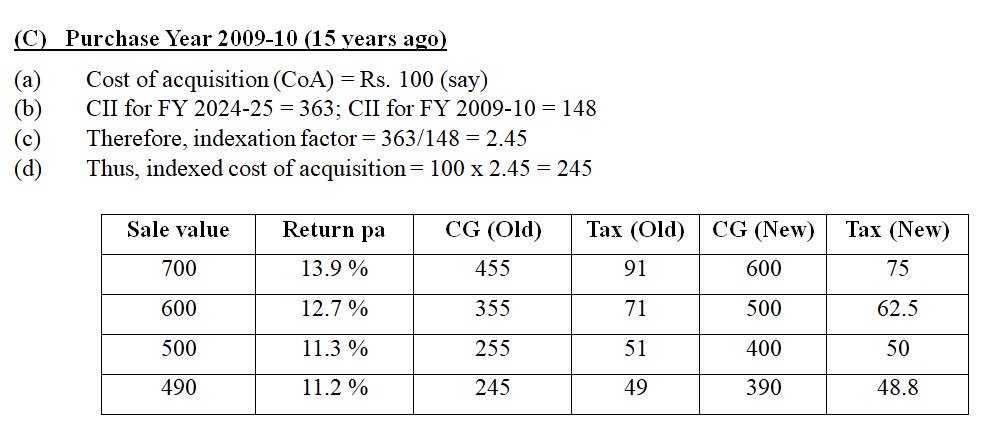

- Nominal real estate returns are generally in the region of 12-16 per cent per annum, much higher than inflation. The indexation for inflation is in the region of 4-5 per cent, depending on the period of holding. Therefore, substantial tax savings are expected to a vast majority of such tax payers. Some cases are given below in this regard to illustrate the tax in both scenarios.

- On investment of capital gain in 54EC bonds (up to Rs. 50 lakh) or in buying or constructing house (up to Rs. 10 crore), the capital gain is exempt from tax, subject to certain specified conditions

- Simplification of any tax structure has benefits of ease of compliance viz computation filing, maintenance of records. This also removes the differential rates for various classes of assets.

Cost Inflation Index:

The Budget 2024’s changes to property taxation have created a complex scenario. While the lower LTCG tax rate is a welcome move, the elimination of indexation benefits has dampened the enthusiasm for property sellers, particularly those who purchased their properties after 2001.

It is essential for property owners to carefully evaluate the implications of these changes before making any decisions related to property sale. Consulting with a tax professional can provide valuable insights and help in optimizing tax planning strategies.

Visit www.cagurujiclasses.com for practical courses