As the income tax return (ITR) filing season is underway in July 2024, with the last date to file ITR for non-audit cases being July 31, it is crucial to understand the recent updates and changes to tax rebates, especially under Section 87A.

Overview of Income Tax Regimes

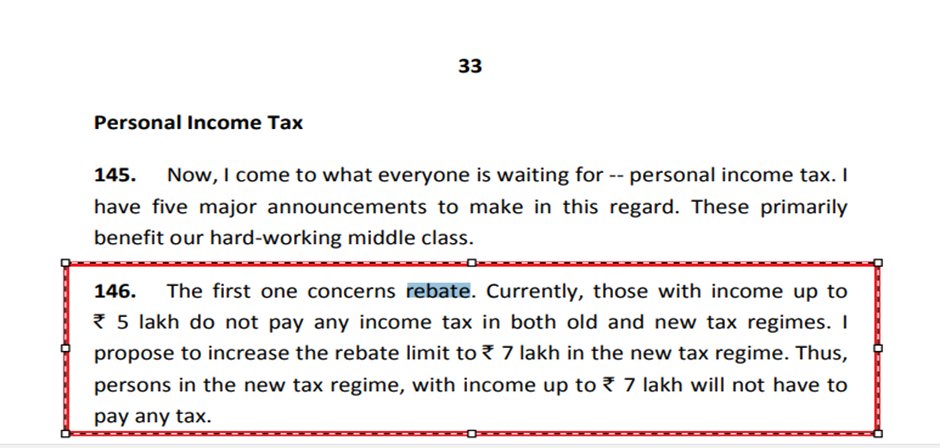

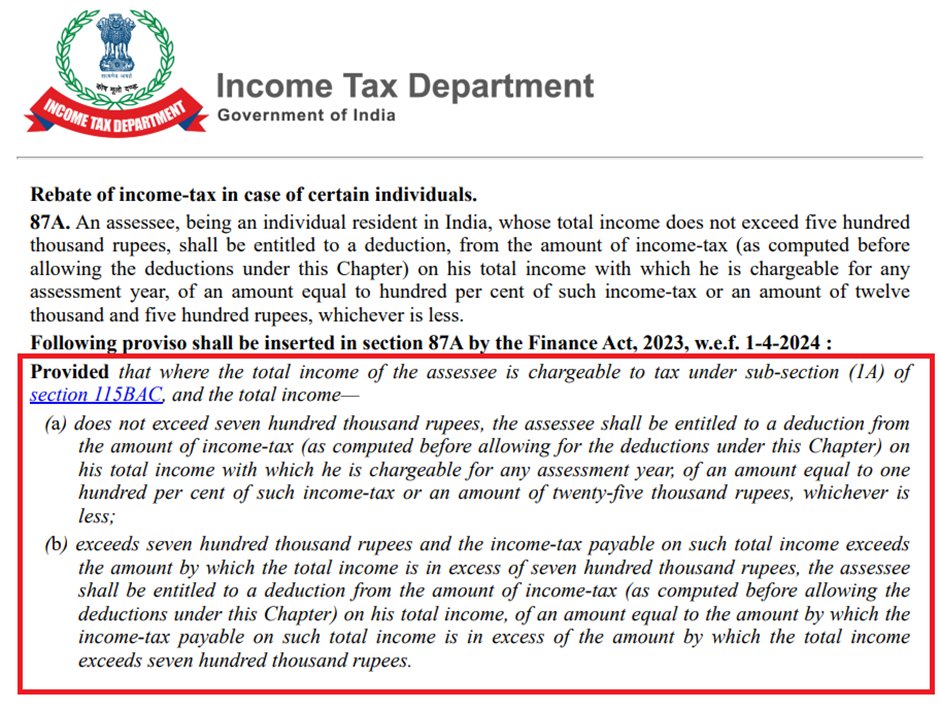

There are two regimes of income tax: the old regime and the new regime. Under the old regime, a rebate under Section 87A is allowed on income up to ₹5 lakh. However, in the new regime, this limit has been increased to ₹7 lakh, as announced in the Union Budget 2023.

Key Changes Post- July 5, 2024 Update

On July 5, 2024, the Income Tax Department updated the ITR utility, which introduced significant changes to the rebate under Section 87A. These changes particularly affect those with special rate incomes such as short-term capital gains (STCG) on shares under Section 111A, long-term capital gains (LTCG), lottery winnings, and income from gaming.

Pre-July 5 Scenario

Before the update, the ITR utility and tax calculator allowed the 87A rebate for STCG under Section 111A and other special rate incomes, except for LTCG under Section 112A, which explicitly restricts the rebate.

Post-July 5 Scenario

After the update, the utility no longer provides the benefit of the Section 87A rebate for special rate incomes, including STCG under Section 111A. This has raised significant concerns and confusion among taxpayers and professionals.

Key Points of Contention

Budget Speech and Memorandum: The Union Budget 2023 speech by the Hon. Finance Minister Nirmala Sitharaman emphasized increasing the rebate from ₹12,500 to ₹25,000 for the new regime, without any additional restrictions. This intention was to extend the benefit without curtailing any existing allowances.

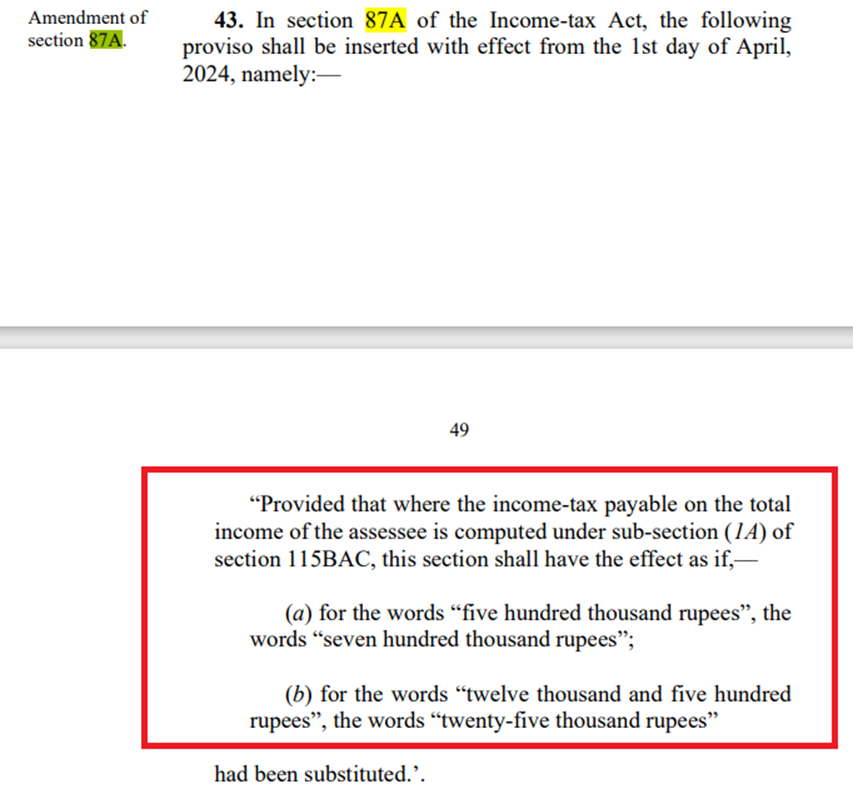

Finance Bill 2023: The initial Finance Bill only proposed changes in the monetary limits, increasing the rebate threshold from ₹5 lakh to ₹7 lakh and the rebate amount from ₹12,500 to ₹25,000. The wording of the final Act, which included provisions for marginal relief, did not intend to restrict already available benefits.

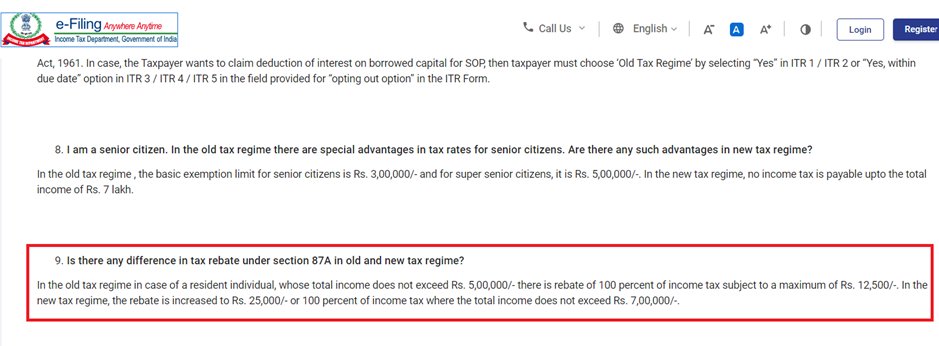

Income Tax Portal FAQs: The FAQs on the Income Tax portal clearly state the increased limit without mentioning any additional differences in the application of Section 87A between the old and new regimes.

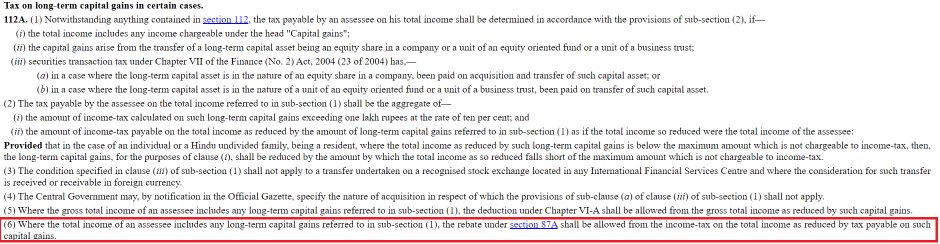

LTCG and STCG: While Section 112A specifically restricts the rebate on LTCG, no such restriction exists for STCG under Section 111A or any other special rate incomes in the new regime.

Interpretation of Total Income: The interpretation by the Department to exclude special rate incomes from the rebate calculation is considered incorrect by many professionals. The concept of total income should be indivisible, and the rebate should apply to the entire total income, including parts taxed at special rates.

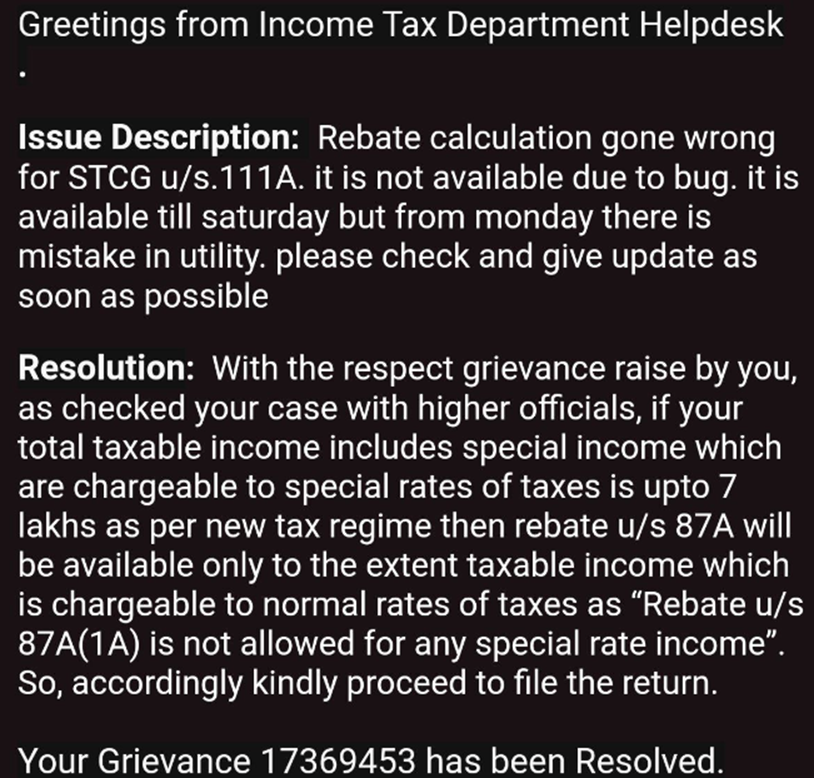

Reply by Income Tax Department

Examples to Clarify the Issue

Consider two scenarios to illustrate the impact of the recent changes:

- Scenario 1: Income up to ₹7 Lakh under the New Regime (Without Special Rate Income)

- If an individual has a total income of ₹7 lakh, they would be eligible for the ₹25,000 rebate under Section 87A, resulting in zero tax liability.

- Scenario 2: Income Including Special Rate Income

- If an individual has a total income of ₹7 lakh, including ₹2 lakh as STCG under Section 111A, the recent changes mean they would not be eligible for the rebate on the special rate income portion. This interpretation would result in a higher tax liability, contrary to the initial benefits intended by the Budget 2023.

Examples of Tax Calculation

Assumptions:

- Tax Rebate under Section 87A before 5th July 2024 is available on total income up to ₹7 lakh including special rate incomes.

- Tax Rebate under Section 87A after 5th July 2024 excludes special rate incomes for the rebate calculation.

Example 1: Normal Income (No Special Rate Income)

| Particulars | Before 5th July 2024 | After 5th July 2024 |

|---|---|---|

| Total Income | ₹7,00,000 | ₹7,00,000 |

| Tax Calculation | ||

| Tax on ₹7,00,000 | ₹25,000 | ₹25,000 |

| Rebate under Section 87A | ₹25,000 | ₹25,000 |

| Net Tax Payable | ₹0 | ₹0 |

Example 2: Income Including STCG under Section 111A (₹2,00,000)

| Particulars | Before 5th July 2024 | After 5th July 2024 |

|---|---|---|

| Normal Income | ₹5,00,000 | ₹5,00,000 |

| STCG under Section 111A | ₹2,00,000 | ₹2,00,000 |

| Total Income | ₹7,00,000 | ₹7,00,000 |

| Tax Calculation | ||

| Tax on Normal Income | ₹10000 | ₹10000 |

| Tax on STCG (15%) | ₹30,000 | ₹30,000 |

| Total Tax Before Rebate | ₹40,000 | ₹40,000 |

| Rebate under Section 87A | ₹25,000 | ₹0 |

| Net Tax Payable | ₹15,000 | ₹40,000 |

Example 3: Income Including Lottery Winnings (₹2,00,000)

| Particulars | Before 5th July 2024 | After 5th July 2024 |

|---|---|---|

| Normal Income | ₹5,00,000 | ₹5,00,000 |

| Lottery Winnings (30%) | ₹2,00,000 | ₹2,00,000 |

| Total Income | ₹7,00,000 | ₹7,00,000 |

| Tax Calculation | ||

| Tax on Normal Income | ₹10000 | ₹10000 |

| Tax on Lottery Winnings (30%) | ₹60,000 | ₹60,000 |

| Total Tax Before Rebate | ₹70,000 | ₹70,000 |

| Rebate under Section 87A | ₹25,000 | ₹0 |

| Net Tax Payable | ₹45,000 | ₹70,000 |

Example 4: Mixed Income Including Both Normal and Special Rate Income

| Particulars | Before 5th July 2024 | After 5th July 2024 |

|---|---|---|

| Normal Income | ₹3,00,000 | ₹3,00,000 |

| STCG under Section 111A | ₹2,00,000 | ₹2,00,000 |

| Lottery Winnings | ₹2,00,000 | ₹2,00,000 |

| Total Income | ₹7,00,000 | ₹7,00,000 |

| Tax Calculation | ||

| Tax on Normal Income | ₹0 | ₹0 |

| Tax on STCG (15%) | ₹30,000 | ₹30,000 |

| Tax on Lottery Winnings (30%) | ₹60,000 | ₹60,000 |

| Total Tax Before Rebate | ₹90,000 | ₹90,000 |

| Rebate under Section 87A | ₹25,000 | ₹0 |

| Net Tax Payable | ₹65,000 | ₹90,000 |

Impact Summary

- Before 5th July 2024: The rebate under Section 87A was available on total income up to ₹7 lakh, including special rate incomes such as STCG and lottery winnings, reducing the net tax payable significantly.

- After 5th July 2024: The rebate under Section 87A excludes special rate incomes from the rebate calculation, resulting in a higher net tax payable for individuals with special rate incomes.

These examples highlight the significant impact of the recent changes on the tax liability of taxpayers with special rate incomes. The exclusion of special rate incomes from the rebate calculation under Section 87A post-5th July 2024 update has increased the tax burden for many taxpayers.

Visit www.cagurujiclasses.com for practical courses

As per the explanation the tax calculation in case of special tax rate under the new regime is exhaustively cleared. But is there any difference considering the special tax rate earning in the old tax regime. Kindly guide the difference in the tax implications vis a vis new tax regime and old tax regime.

This article will be beneficial for everyone, even those who are (junior) CAs or non-CAs who file ITR of assessees. Even, I think that the Income Tax Department staff should also read such texts of yours. Even at the age of 65, I continue to study such topics every day. I pray to God for more and more progress in your organisation as well as of your entire team members.

Hello Mam,

In my opinion & interpretation of reply given by the department, 87A rebate in case of total income is upto 7L & includes Special rate income then rebate will be allowed only to the extent of income taxed under normal slab rate. Accordingly in the Example.2 rebate on 5L i.e. Rs. 10000 will be given and Tax on STCG of Rs. 30,000/- shall be net payable.

Same logic goes in the further examples also . So in my opinion net payable in example 2 will be 30000 & in example 3 will be 60000.

Kindly correct me if my interpretation is incorrect

Thank you

Hello Mam,

In my opinion & my interpretation of the reply given by the department, in case total income includes any income taxed @ special rate, then 87A rebate will allowed to the extent of income taxable @normal slab rate.

Accordingly, in your exmaple-2, for the income of 5 lakhs, 87 rebate will be allowed and the tax on STCG of Rs. 30000 will be net tax payable and the same goes with example -3 wherein 60000 will be net tax payable.

Kindly let me know if my interpretation is incorrect.

Thanking you.

Hello Mam,

In my opinion & my interpretation of the reply given by the department, in case total income includes any income taxed @ special rate, then 87A rebate will allowed to the extent of income taxable @normal slab rate.

Accordingly, in your exmaple-2, for the income of 5 lakhs, 87 rebate will be allowed and the tax on STCG of Rs. 30000 will be net tax payable and the same goes with example -3 wherein 60000 will be net tax payable.

Kindly let me know if my interpretation is incorrect.

Thanking you